World’s leading reporting organizations discussing alignment

Renewable Energy Followers 18th Jihoon Oh

With the outbreak of COVID-19, global interest on ESG increased massively as many would agree. ESG which classifies factors related to sustainablity into three measures (Environment, Social, Governance) was first introduced to public for information users to assess a company or organization with a different perspective compared to traditional measurements. Thus, as global interest on ESG increases, now various corporations consider ESG as a standard which will aid on corporate sustainability and managing risks. Since ESG mostly consists with non-financial information, companies and organizations need exact framework for clear disclosure and strategies. Before these needs, considerations related to non-financial disclosure about corporate sustainability have been already discussed on major institutions including GRI (Global Reporting Initiative), IIRC (International Integrated Reporting Council), SASB (Sustainability Accounting Standards Board), CDP(Carbon Disclosure Project), CDSB (Climate Disclosure Standards Board).

So what is Sustainable Reporting Framework? Sustainable Reporting Framework stands in order to help organizations setting goals and measuring results to achieve sustainablity. Since matters related to ESG are sometimes theoretical, organizations need real-life measurements. However, there are variety of objectives on sustainability with dynamic nature of topics which makes it hard for companies to report. For their needs, various institutions developed Sustainable Reporting Framework. However, since there are so many frameworks developed by various institutions and organizations, it is hard for companies to choose which framework to follow creating confusions.

And on September 2020, five framework and standard setting institutions (GRI, SASB, IIRC, CDSB, CDP) announced ‘Statement of intent to work together towards comprehensive corporate reporting’. The statement shows user and objectives of sustainability disclosure, emerging demand of comprehensive standards, vision for sustainability disclosure and other topics.

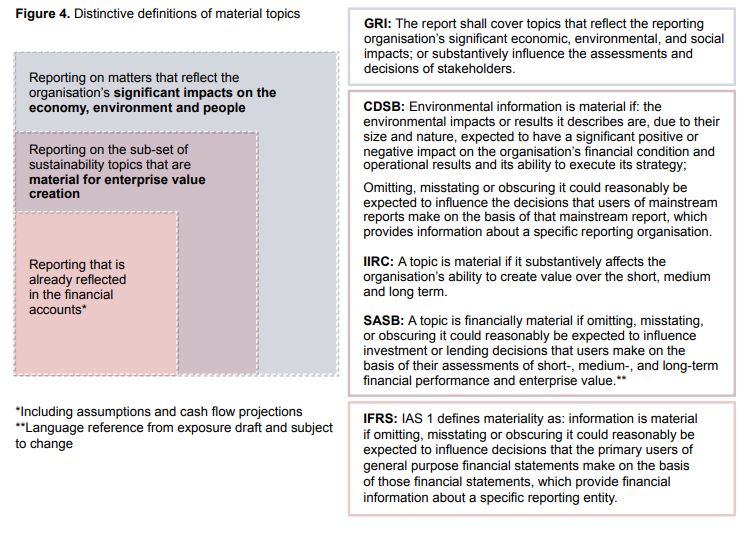

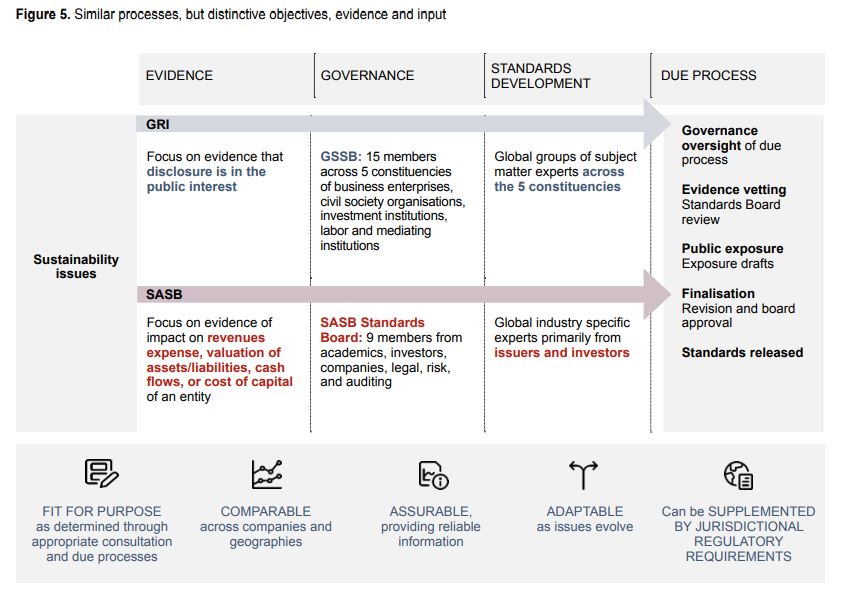

Considering each standard, standards from each institution vary since they have distinctive definitions of material topics, objectives, evidence and input.

[Material 1. Distinctive definitions of material topics ]

[Material 2.Similar process, but distinctive objectives, evidence and input]

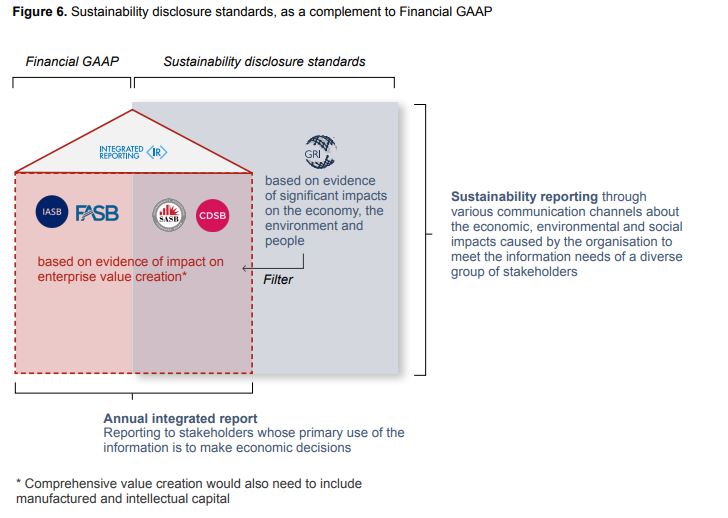

Because of these differences, the goal of comprehensive corporate reporting system is to provide more complete and comparable information to companies’ different stakeholders. Thus, enabling disclosure that is relevant to enterprise value creation enabling various communications at the same time. The Hosue below shows how each sustainability disclosure standards will be integrated while complementing Financial Generally Accepted Accounting Principle and also satisfying the demand of stakeholders.

[Material 3. Sustainability disclosure standards, as a complement to Financial GAAP ]

With global interest on ESG including individual level, corporate level and national level, the world is changing fast for sustainable future. It is time for us to open our eyes towards various perspectives including sustainability.

지속가능보고서 에 대한 대학생신재생에너지기자단 기사 더 알아보기

1. " 지속가능보고 공시표준, 통합되나", 18기 오지훈, https://renewableenergyfollowers.tistory.com/3525?category=745296

참고문헌

1) Integrate reporting, "Statement of Intent to Work Together Towards Comprehensive Corporate Reporting", 2020.9, https://www.integratedreporting.org/resource/statement-of-intent-to-work-together-towards-comprehensive-corporate-reporting/

2) 박란희 chief editor, "GRI, SASB 등 글로벌 표준 빅5 뭉쳤다", 임펙트온, 2020.09.23, http://www.impacton.net/news/articleView.html?idxno=543

GRI, SASB 등 글로벌 표준 빅5 뭉쳤다 - IMPACT ON(임팩트온)

GRI와 SASB 등 비재무정보(ESG) 공시 표준을 정하는 5개기관이 협업하기로 11일(현지시각) 성명서를 발표했다. 이는 비재무공시의 글로벌 표준 작업을 위한 첫 단추를 꿰었다는 평을 받고 있다.이번

www.impacton.net

'News > 기술-산업-정책' 카테고리의 다른 글

| 고쳐 쓰는 건축, 그린 리모델링 (14) | 2021.11.29 |

|---|---|

| 지속가능보고 공시표준, 통합되나 (3) | 2021.11.07 |

| Kyoto Mechanism and Paris Agreement, what’s the difference? (0) | 2021.10.29 |

| 2020년까지 적용된 교토체제와 앞으로 적용될 파리기후체제에 대하여 (3) | 2021.10.25 |

| 기후위기 피해자인 미래세대는 언제까지 무시받나 (4) | 2021.10.25 |

댓글